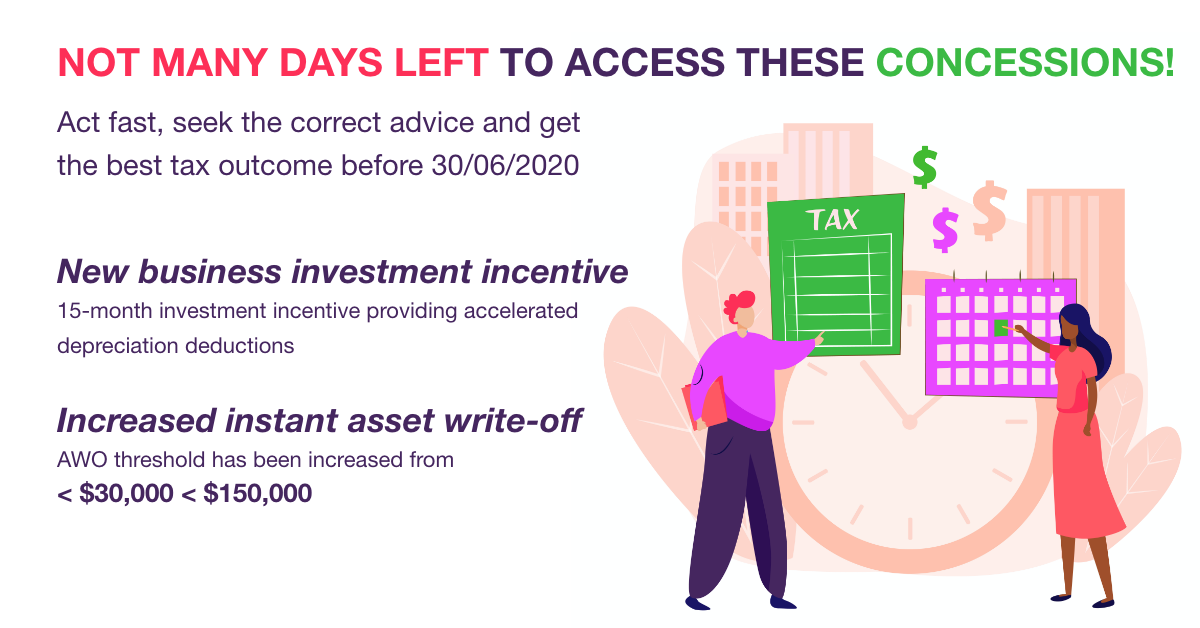

Not many days left to access these concessions!

Get ready – second round of cash flow boosts

June 25, 2020

New business investment incentive

15-month investment incentive providing accelerated depreciation deductions

Key features:

- Deduct 50%of the cost of an eligible asset on installation, with existing depreciation rules applying to the balance of the asset’s cost

- Eligible businesses — aggregated turnover less than $500m♣Eligible assets —new assets that can be depreciated under Div 40

- Acquired after the date of the announcement, 12 March 2020, and first used or installed by 30 June 2021

- Does not apply to second-hand assets, or buildings and other capital works depreciable under Div 43

- Car limit of $57,581 still applies

Increased instant asset write-off

- AWO threshold has been increased from < $30,000 to< $150,000

- Aggregated annual turnover for eligibility has been increased from < $50m to < $500m

- Applies from the date of the announcement, 12 March 2020, until 30 June 2020

- Applies to new or second-hand assets first used or installed ready for use in the above period

- From 1 July 2020, the IAWO threshold will revert to the original $1,000 for SBEs (turnover < $10m)

Important:

- Acquisition date for SBEs— 7:30 pm on 12 May 2015 to 30 June 2020

- Acquisition date for MBEs— 7:30 pm on 2 April 2019 to 30 June 2020

- Acquisition date for LBEs— 12 March 2020 to 30 June 2020

{kind=link}